There Is No Market

Refuting a common misconception about US Healthcare

A prominent X account recently posted her insane $9,000 bill for a hospitalization from a year prior.

Then, as always happens, someone on the internet announced with great confidence that this is what happens when healthcare is left to the free market.

As if the most regulated industry in America actually functions in a free market.

American healthcare contains private actors, but private actors alone do not make a market. Doctors, nurses, hospital executives, private insurers, private equity firms, billing companies, pharmacy benefit managers, and nonprofit health systems all pursue revenue. Of course they do. That is not the interesting question. The interesting question is why the rules reward the behavior they reward. Why does hospital ownership make the same outpatient service more expensive? Why does a physician need a billing code before a service gets reimbursed? Why does a hospital hire armies of documentation specialists to extract the right words from a chart? Why can a patient with “coverage” still be unable to obtain care? Why does every reform seem to produce another layer of compliance staff?

Because we do not have a free market, or anything even close.

American healthcare is a government-built payment machine. Before Medicare became the dominant payer and pricing reference point, physicians and patients had more room to experiment with direct payment, prepaid arrangements, fraternal society models, early Blue Cross-style coverage, cash practice, and other local contracting forms. There was room for prices and contracts to emerge from relationships between patients, physicians, hospitals, employers, and communities.

Medicare standardized and federalized that world. It took physician services and forced them into a strict fee-for-service architecture using CPT codes, RVUs, documentation rules, and federal conversion factors. It replaced hospital prices with DRGs, prospective payment formulas, outpatient payment classifications, and facility fees. It then made participation in that system nearly unavoidable through billing rules, coverage rules, Conditions of Participation, and regulatory control over hospitals. After that, government policy protected the incumbents through certificate-of-need laws, physician-owned hospital restrictions, Stark and Anti-Kickback complexity, site-of-service differentials, hospital subsidies, and tax preferences.

Private actors behave badly inside this system, but they are responding rationally to rules government created. Hospitals consolidate because payment rules reward consolidation. Physicians sell to hospitals because independent practice is punished. Insurers build administrative barriers because tax-favored and government-entrenched third-party payment removed price discipline. Patients receive absurd bills because nobody ever had to give them a real price.

The first distortion: insurance through your employer

The original sin of American healthcare financing is the employer-sponsored insurance tax exclusion. Employer-paid premiums for health insurance are excluded from federal income and payroll taxes, and the portion of premiums employees pay is typically excluded from taxable income as well. That exclusion lowers the after-tax cost of employer-sponsored coverage and helps explain why most American families with private insurance get coverage through work. The IRS is explicit that the value of the employer’s excludable contribution to health coverage remains excluded from an employee’s income and is not taxable.

That sounds technical, but the effect is enormous. The tax code makes health insurance purchased through an employer more favorable than cash wages. If your employer pays you an additional dollar in wages, that dollar is taxed. If your employer uses compensation dollars to buy health insurance, that benefit is tax advantaged. Over time, this pushed health insurance into the workplace and made the employer the central purchaser of coverage.

The distortion is subtle because workers often think their employer “gives” them health insurance. But employers do not create compensation out of charity. Health benefits are part of total compensation. Workers pay for employer-sponsored insurance through lower wages.

This matters because markets depend on visible tradeoffs. In ordinary life, a consumer can decide whether a more expensive product is worth the money. But in employer-sponsored insurance, the patient is not really the customer. The employer typically chooses the plans available to the employee. The employee often has only a few plans from which to choose. When the employee changes jobs, the insurance changes too. Patients lose continuity because coverage is tied to employment rather than to the person.

This also creates a massive hidden subsidy to the healthcare industry. Because employer-sponsored insurance is tax-favored, workers are nudged toward compensation in the form of health benefits rather than wages. That encourages more dollars to flow through insurance than would flow if patients were spending their own after-tax money. It also encourages overinsurance. Routine care, predictable care, and relatively inexpensive care get pushed through an insurance product that was originally supposed to protect against catastrophe.

Once that happens, the patient stops acting like a normal buyer. The patient does not ask, “What does this cost, and is it worth it?” The patient asks, “Is it covered?” The physician does not simply quote a price. The physician documents, codes, and submits a claim. The insurer does not merely insure against rare catastrophe. It becomes a payment intermediary for ordinary healthcare consumption. EThe patient is left with premiums, deductibles, copays, coinsurance, networks, and surprise bills.

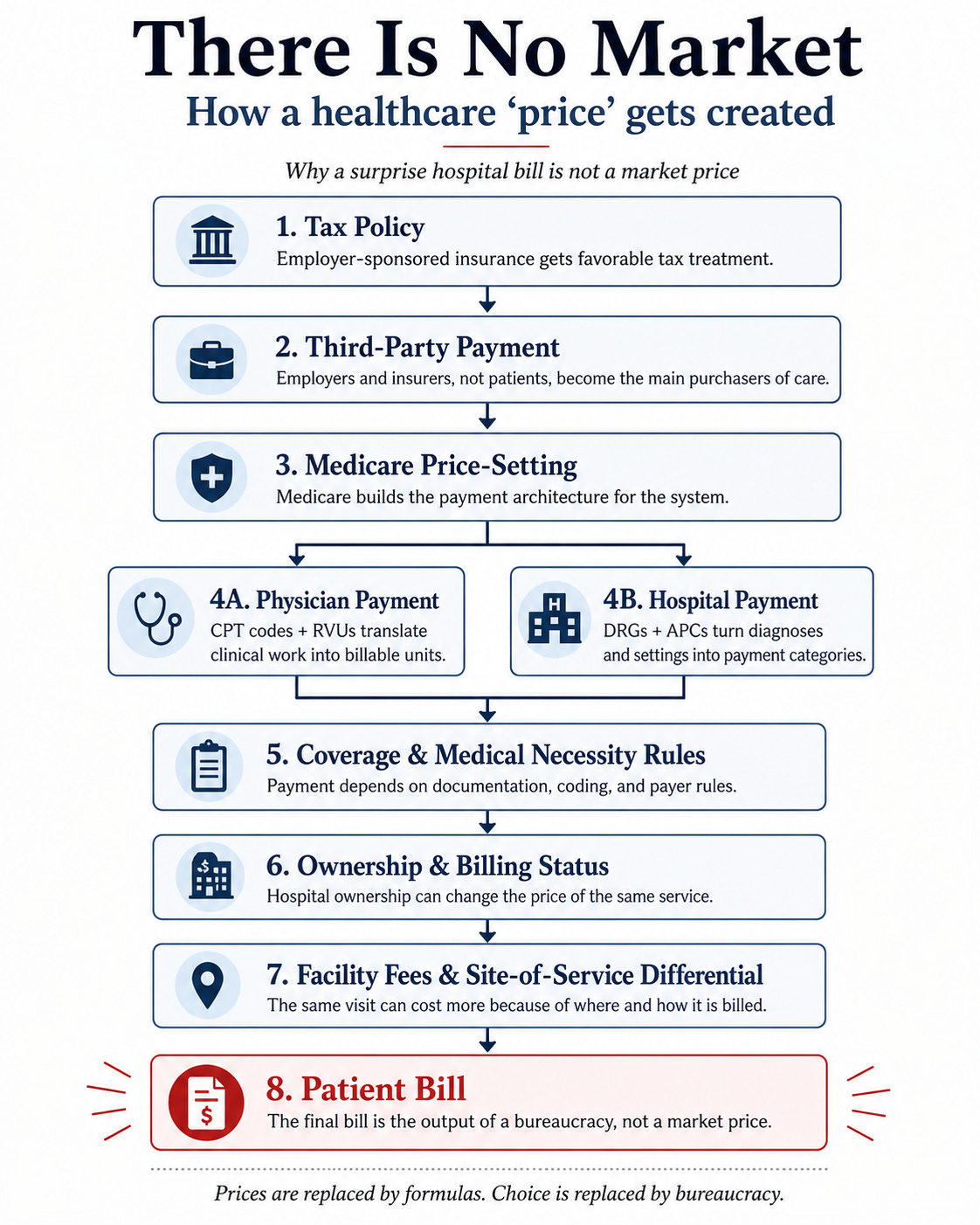

Medicare did not just insure seniors. It built the pricing machine.

Medicare is usually discussed as an insurance program for older Americans and certain disabled patients. That is true, but incomplete. Medicare did not merely create a payer. It created the central pricing architecture of American healthcare.

Medicare entrenched fee-for-service as the dominant federal payment architecture. That did not merely determine how the government paid claims. It reshaped the entire market around claims submission, coding, documentation, coverage rules, and compliance. Creative contracting did not disappear entirely, but it was pushed to the margins. The default became simple: if a service is covered by Medicare, it must be translated into a billable code and paid according to the federal pricing machine.

For physicians, Medicare pays through the Physician Fee Schedule. CMS describes PFS payment rates as being based on relative value units for physician work, practice expense, and malpractice expense. Those RVUs are converted into payment rates through a fixed-dollar conversion factor and adjusted geographically.

Pause on that.

A physician does not simply tell a patient, “Here is what my judgment, skill, time, and availability cost.” The physician submits a code. That code has assigned RVUs. Those RVUs are set by CMS, adjusted by geographic factors, and converted into dollars by a federal conversion factor. The economic reality of the clinical encounter depends on whether the work fits the code, whether the diagnosis supports medical necessity, whether the documentation satisfies the rules, and whether the claim survives the payment process.

In normal professional markets, a lawyer, accountant, architect, or consultant can define a service, quote a fee, and contract directly with a client. In Medicare medicine, clinical work must first be translated into billing language, and the price is set by the government. The code becomes the economic product.

A new procedure may be clinically useful, but if there is no clean CPT code, the payment pathway is uncertain. The physician may use an unlisted code, which invites manual review, denial, inconsistent payment, and administrative friction. A service may have a code but still be denied because the diagnosis code does not justify it. A physician may perform valuable cognitive work that is hard to map onto a billable category and therefore becomes economically invisible. Documentation grows not because the patient needs a longer note, but because the billing machine needs proof.

Medicare did not create a marketplace for physician services. It created a translation system in which clinical work must be converted into codes before it can become money.

RVUs are price-setting with a medical vocabulary

The RVU system is often discussed as if it were technical, neutral, and somehow natural. It is not. It is price-setting.

CMS assigns relative values to services. Those values attempt to reflect physician work, practice expense, and malpractice expense. The RVUs are then converted into dollars. This is not a market discovering prices through exchange. It is an administrative process estimating value from inputs.

There is something almost comical about the philosophical structure of it. The system tries to measure the “value” of physician work by estimating labor time, intensity, overhead, and relative resources. We have a healthcare payment system that, at least in spirit, often resembles an administered labor theory of value. If the service takes more physician time, it may be worth more. If the estimated time falls, the service may be worth less. If a procedure becomes faster because physicians improve their technique, the bureaucratic instinct is to revalue the code downward.

A real market rewards efficiency. If a surgeon develops a better way to do something, and patients value that surgeon’s skill, the surgeon may benefit. In an administered pricing system, improved efficiency can become evidence that the service should be paid less.

It also changes the politics of medicine. Physicians and specialties end up fighting over relative valuation. The question becomes not, “What do patients value?” but, “What does the fee schedule recognize?” The unit of concern is no longer the patient’s willingness to pay for skill, access, trust, speed, or outcome. It is the code, the RVU, and the conversion factor.

Once Medicare built this skeleton, commercial insurers did not create a parallel free market. They used Medicare as a reference point, sometimes paying a percentage of Medicare, sometimes using similar coding logic, sometimes layering their own rules on top.

Hospital inpatient payment: the diagnosis becomes the product

Hospitals have their own version of administered pricing. Medicare’s Inpatient Prospective Payment System pays hospitals using diagnosis-related groups, or DRGs. CMS explains that each DRG has a payment weight based on the average resources used to treat Medicare patients in that DRG. Under IPPS, Medicare pays for inpatient hospital services on a rate-per-discharge basis that varies according to the DRG assigned to the beneficiary’s stay.

Again, that is price-setting.

A hospital admission does not have a market price in the ordinary sense. The patient does not shop for a DRG. The doctor does not negotiate a DRG with the family. The hospital documents and codes the admission into a federal classification system. Payment depends on the principal diagnosis, additional diagnoses, procedures, and other factors. CMS states that the MS-DRG classification is based on the information reported by the hospital, including the principal diagnosis, additional diagnoses, and procedures performed during the stay.

In an ordinary clinical world, the chart should communicate what happened to the patient, what the physician thought, what the plan is, and what needs to happen next. Under DRGs, the chart also becomes a revenue instrument. The words selected in the note matter financially. “Pneumonia” may pay differently than “pneumonia with acute hypoxic respiratory failure.” “Confusion” may pay differently than “encephalopathy.” “Poor intake” may pay differently than “severe malnutrition.” “Kidney numbers bumped” may pay differently than “acute kidney injury.”

Some of this is legitimate severity capture. Hospitals treating sicker patients should not be paid as if they treated healthier ones. But the incentive is obvious. Once diagnosis codes change payment, diagnosis coding becomes a business function. Hospitals hire clinical documentation improvement teams. Physicians receive queries. Administrators worry about CCs and MCCs. The chart becomes a battleground between clinical reality, billing specificity, compliance risk, and revenue optimization.

The patient did not become sicker because a new word appeared in the note. The payment formula changed because the documentation became more favorable.

This is one of the most important distortions in modern hospital medicine. It gives enormous power to administrative systems that sit between the bedside and the bill. It also pollutes medical records. Patients accumulate diagnoses that may have been entered to satisfy a payment or documentation rule. Future doctors inherit charts full of billing artifacts. The clinical record becomes longer, less readable, and less trustworthy.

Then we wonder why doctors spend so much time staring at screens.

Outpatient hospital payment: ownership becomes destiny

If you thought the inpatient side was bad, look at how outpatient care distorts the market.

CMS pays hospital outpatient departments under the Outpatient Prospective Payment System. Under OPPS, items and services are assigned to Ambulatory Payment Classifications, which group services that are similar clinically and in resource use. OPPS payments are made for items and services furnished by hospital outpatient departments.

This creates a separate payment pathway for hospital outpatient care. That pathway often pays differently than care delivered in an independent physician office or ambulatory surgical center.

Yet outpatient hospital care and independent physician care are often indistinguishable. Suppose you go in for a regular clinic visit in an independent doctor’s office. It gets paid under the physician fee schedule. If a hospital buys that office and nothing else changes, it can become a hospital outpatient department using a different payment system.

Same doctor. Same patient. Same exam room. Same echocardiogram, infusion, clinic visit, or minor procedure. But after the hospital buys the practice or facility, the service may be billed as hospital outpatient care. A facility fee appears, and the cost rises.

That rewards hospitals for acquiring outpatient care. It punishes independent practices that deliver the same services without the hospital billing apparatus.

MedPAC has repeatedly discussed site-neutral payment because Medicare itself pays differently across ambulatory settings for similar services. In its March 2026 report, MedPAC wrote that there remain opportunities to expand site-neutral policies to align Medicare payment rates for similar services across ambulatory settings. It estimated that applying site-neutral payments to 15.6 million elective clinic visits in on-campus hospital outpatient departments would have decreased fee-for-service Medicare payments by about $1.1 billion in 2024.

If the price difference were simply a market price reflecting better care, why would site-neutral payment be an issue at all? The very existence of the site-neutral debate is an admission that Medicare’s payment rules pay different amounts based on where and how a service is billed, not merely what was done for the patient.

Hospitals understand this. That is why they are growing like insatiable beasts, devouring independent practices. They are not irrational. They are following the rules. If government pays more when the hospital owns the outpatient setting, hospitals will buy outpatient settings.

Medicare made escape difficult

At this point, someone might say: fine, Medicare is administered pricing. But why not let doctors and patients contract around it? Why not let hospitals and patients build alternative arrangements? Why not let people choose direct payment, transparent bundles, subscription models, physician-led facilities, or cash prices?

Because Medicare does not merely choose one payment method among many. It made its chosen method the default operating language of American medicine.

Medicare participation is a legal status. CMS states that Medicare participation means a physician or supplier agrees to accept assignment on all claims for Medicare-covered services, accept Medicare-allowed amounts as payment in full, and not collect more from the patient than the deductible, coinsurance, or copayment.

Once a service is covered by Medicare, the physician and patient are no longer simply free to create their own arrangement. The service must fit Medicare’s rules. The physician must either participate, accept assignment, submit claims, obey coverage and documentation requirements, and accept Medicare’s allowed amount, or formally opt out of Medicare altogether. A physician can opt out, but opting out is a formal legal pathway with private contracting requirements and major practice implications. It means opting out of Medicare payments, severely limiting the ability of that doctor to care for patients in many settings outside a highly selective elective practice.

It is not the same as a normal professional saying, “Here is my fee.”

For hospitals, escape is even less realistic. A hospital that wants to serve older patients, disabled patients, Medicaid patients, commercially insured patients whose plans expect Medicare participation, or communities that view Medicare access as essential cannot simply opt out of the Medicare operating system. Medicare is too large, too embedded, and too central to the hospital business model.

CMS says Conditions of Participation and Conditions for Coverage are the requirements healthcare organizations must meet to begin and continue participating in Medicare and Medicaid. For hospitals specifically, CMS states that 42 CFR Part 482 contains the health and safety requirements hospitals must meet to participate in the Medicare and Medicaid programs.

Some of these rules are necessary. No serious person wants hospitals without basic safety standards. But the larger point is that Medicare participation becomes operational control. Medicare does not merely say, “Here is what we will pay.” It says, “If you want access to the dominant public payer, your hospital must operate under our conditions.”

Those conditions touch medical staff structure, nursing services, patient rights, quality assessment, infection control, discharge planning, records, emergency preparedness, and hospital governance. Over time, hospitals build entire administrative infrastructures around compliance. Accreditation readiness, policy management, documentation protocols, quality committees, survey preparation, regulatory affairs, and internal auditing become part of the cost structure of care.

This is the missing point in most debates about healthcare markets. Medicare is not just a payer. It is a licensing-adjacent governing structure. A hospital that wants to participate in Medicare and Medicaid must organize itself around Medicare’s rules. Those rules become hospital policy with all the required compliance infrastructure and cost. Then, when patients complain that healthcare is expensive, policymakers blame the market.

This is why “just pay cash” is not a serious answer at scale. Cash-pay primary care, direct specialty care, transparent surgical bundles, and employer direct contracting can work around the edges, and I strongly support them. But Medicare’s architecture makes large-scale escape difficult. For covered services involving Medicare beneficiaries, the doctor-patient transaction is constrained. For hospitals, participation brings conditions that shape the entire institution. For new facilities, ownership and entry rules often block competition before it starts.

Medicare did not just create public insurance. It extinguished many of the pathways by which alternative markets might have emerged. Doctors used to enter into creative financing arrangements. Not just cash pay, but prepaid care, monthly memberships, capitation-like arrangements, fraternal society contracts, and other local agreements. Many of the arrangements we might have seen never had a chance to mature because federal healthcare policy chose a different path: fee-for-service claims processed through a federal pricing machine.

The state protected the incumbents

Once government replaced prices with formulas and made escape difficult, the next layer was incumbent protection.

Certificate-of-need laws are the clearest example. In many states, new facilities or services require government approval before they can be built or expanded. Existing hospitals can object to new competitors. The language is always about planning, avoiding duplication, preserving access, and protecting community resources. The economic effect is often incumbent protection.

Imagine needing Ford’s permission to open a Toyota dealership. Imagine Starbucks being allowed to object before an independent coffee shop opens across the street. We would immediately recognize this as anticompetitive.

Certificate-of-need laws give existing institutions a political tool to fight competitors without having to compete on price, access, efficiency, or patient experience.

Then there are physician-owned hospital restrictions.

CMS explains that Section 6001 of the Affordable Care Act amended the rural provider and whole hospital exceptions so that a hospital with physician ownership or investment may not increase the number of operating rooms, procedure rooms, and beds beyond its baseline capacity.

Hospitals can own physicians. Physicians are restricted from owning hospitals.

This is one of the most revealing features of American healthcare policy. We are told physician ownership is dangerous because doctors might profit from the facilities to which they refer. That concern is not imaginary. Incentives matter. But then we allow hospitals to employ physicians, buy practices, capture referrals, bill facility fees, steer patients internally, and use their market power to negotiate higher rates.

If the goal were truly neutral competition, the law would care about transparency, conflicts of interest, outcomes, and patient choice regardless of who owns the facility. Instead, the rules suppress physician-led competition while allowing hospital-led consolidation.

Stark Law and the Anti-Kickback Statute add another layer. The anti-corruption rationale is real. Nobody wants sham referrals, kickbacks, or abusive self-dealing. But complexity has consequences. The more complicated the rules, the more the system favors institutions large enough to hire lawyers, compliance officers, consultants, and administrators to navigate them. Large hospital systems can structure arrangements, absorb legal costs, and manage regulatory risk. Large hospital systems are exempt from self-referral restrictions. Independent physicians are not.

That is how consolidation happens in practice. Not because hospitals are always more efficient. Not because patients demanded hospital ownership of everything. But because the regulatory environment favors scale. The hospital can afford the compliance department. The independent practice cannot. The hospital can survive payment delays and denials. The independent practice cannot. The hospital can monetize facility fees and outpatient payment differentials. The independent practice cannot. The hospital can capture subsidies. The independent practice cannot.

Then, when independent doctors sell, policymakers call it integration.

Subsidies turned hospitals into payment-channel machines

Hospitals are not normal firms selling a service to customers at visible prices. They are institutions embedded in a dense web of public payment streams and policy subsidies.

Some of these subsidies have defensible goals. Graduate medical education payments support teaching hospitals. DSH and uncompensated care payments support hospitals caring for low-income patients. Medicaid supplemental payments and state directed payments may help safety-net institutions survive. The 340B drug program was designed to help covered entities stretch scarce resources.

Once hospitals receive large streams of revenue through public formulas, discounts, supplemental payments, and designations, financial survival becomes partly clinical and partly political. Hospitals learn to master payment channels. They hire consultants to optimize revenue. They lobby over formulas. They acquire service lines that create favorable reimbursement. They build finance teams around DSH, GME, 340B, provider taxes, directed payments, and outpatient facility billing.

In a normal market, a firm survives by offering a product customers value at a price they are willing to pay. In hospital healthcare, survival often depends on mastering a maze of public payment programs. The patient may still matter morally and clinically, but financially the patient is often the vessel through which codes and governmental revenue flows.

The 340B drug discount program is a particularly clear example. Under 340B, covered entities can purchase outpatient drugs at discounted prices. HRSA describes the program as allowing covered entities to stretch scarce federal resources as far as possible, reaching more eligible patients and providing more comprehensive services. The stated purpose sounds noble. But discounted drug acquisition combined with reimbursement based on payer arrangements can create powerful spread opportunities. Hospitals that qualify for 340B have incentives to acquire physician practices, move drug administration into hospital outpatient departments, and capture both drug economics and facility payments.

If we pay hospitals more when they own outpatient care, hospitals will own outpatient care. If we give hospitals access to drug spreads when they acquire infusion volume, hospitals will acquire infusion volume. If we restrict physician-owned competitors, hospitals will face fewer physician-led alternatives. If we route supplemental dollars through complex public formulas, hospitals will invest in mastering those formulas.

In the end, many hospitals learn that the highest-margin activity is not simply providing better care. It is mastering arbitrage: site-of-service arbitrage, drug-spread arbitrage, subsidy capture, documentation capture, and regulatory positioning. Patient care remains the moral reason the institution exists, but the financial machinery increasingly rewards everything around the care rather than the care itself.

Value-based care did not restore the market

At some point, policymakers recognized that fee-for-service has obvious problems. Paying for units of activity can reward volume. It may not reward outcomes. It can encourage overuse. These are real concerns.

But the policy response was not to restore prices, competition, consumer choice, and direct accountability. The response was to create another layer of government-designed metrics.

Value-based care sounds market-like because it uses words such as value, quality, accountability, and outcomes. In practice, it often just makes more formulas for hospitals to game and more regulatory burdens for doctors to endure.

CMS describes hospital value-based programs as linking payment to quality and value, including programs such as Hospital Value-Based Purchasing, the Hospital Readmissions Reduction Program, and the Hospital-Acquired Condition Reduction Program. Physician programs such as MIPS, accountable care organizations, bundled payments, episode-based measures, risk adjustment, and quality reporting all operate through definitions set by government or payer administrators.

Of course, quality matters enormously. The problem is that measured metrics are not the same as quality. Once payment depends on metrics, institutions manage metrics.

Readmission penalties can punish hospitals caring for poorer and sicker patients. Fall metrics can lead to bed alarms, immobility, and risk aversion. Infection metrics can create documentation battles. Bundled payments can penalize surgeons who take care of complex patients. ACOs can reward benchmark strategy, coding intensity, attribution management, and patient selection. MIPS can force physicians to report measures that have little to do with what patients actually value.

Value-based care replaces price signals with federal metrics. It asks CMS to define value from the top down, then acts surprised when hospitals and physicians learn to optimize the definitions.

Hayek would not be surprised. Central planners always lack the dispersed knowledge embedded in real transactions. They cannot know every patient’s preferences, every physician’s judgment, every local constraint, every family’s tradeoff, every hospital’s operational reality, every difference between a straightforward case and a disaster waiting to happen. So they create measures, which, tied to payment, dictate behavior.

The absurdity of calling this capitalism

At this point, look at the machinery we have described.

The tax code pushes insurance through employers. Medicare sets physician prices through CPT codes, RVUs, and conversion factors. Medicare sets inpatient hospital prices through DRGs and prospective payment. Medicare sets outpatient hospital prices through OPPS, APCs, and facility fees. Medicare participation constrains direct contracting. Conditions of Participation turn payment into operational control. Certificate-of-need laws protect incumbent hospitals. Physician-owned hospital restrictions suppress physician-led competition. Stark and Anti-Kickback complexity favor large compliance-heavy systems. Hospital subsidies reward mastery of public payment channels. Value-based care adds metrics, reporting, attribution, risk adjustment, and administrative overhead.

Then a patient gets a ridiculous bill and someone says, “This is the free market.”

A market is not defined by the mere presence of private organizations. If private firms operate inside a government-designed price system, respond to government-created subsidies, comply with government participation rules, and exploit government-protected barriers to entry, then what you have is not a free market. It is a regulated cartel with private revenue-maximizing behavior inside it.

If you think American healthcare is expensive because the market is too free, your solution will be more central control: more price-setting, more metrics, more reporting, more subsidies, more rules, more federal demonstration projects, more committees, more compliance. But much of the current mess was created by exactly those tools.

Medicare price-setting did not eliminate the need for prices. It replaced real prices with formulas. Value-based care created new games. Facility payment rules rewarded hospital acquisition. Subsidies made hospitals dependent on political finance.

The more government suppresses real market signals, the more administrators must invent substitutes. That is the system we have built.

What a real market reform would require

A serious market-oriented healthcare reform would not pretend that healthcare is identical to buying coffee. But it does not require the centrally planned system we have now.

Real reform would start by restoring the basic conditions of a market wherever they can exist. There billions of elective, low-cost clinical transactions each year, from outpatient clinic visits, labs, x-rays, and minor procedures.

Patients should know prices before care whenever possible. Independent physicians, ASCs, and physician-owned hospitals should be allowed to compete on even footing. Medicare beneficiaries should have more freedom to use their own money for care without forcing physicians into all-or-nothing participation choices. Safety-net support should fund patients more directly instead of feeding the incumbent hospital system.

The point is not that markets solve every problem. The point is that we have spent decades suppressing market signals and then blaming markets for the consequences.

There are patients, doctors, hospitals, insurers, and employers trapped inside a government-designed payment machine.

The $9,000 surprise bill is not what happens when the free market runs wild.

It is what happens when the market has been regulated, coded, subsidized, consolidated, and administered out of existence.

Edit needed: “EThe patient is left with premiums, deductibles, copays, coinsurance, networks, and surprise bills.”

I have experienced this only as a programmer in the healthcare industry for 19 years realizing that a small fraction of what I did actually helped doctors take care of patients. It was soul crushing, but clearly I was only on the fringes of the full horror.

Healthcare needs far, far less government, but people think “reform” always means more government. So here we are.